As an Indian trader you must have heard the word “margin” quite a few times. But what is the margin? Why is it so important? And how do you know how much margin you need for each trade, especially when trading indices?

If these questions sound familiar, you’re in the right place. This margin requirement guide breaks everything down in a simple way—what margin really is, how margin per lot works, and the latest index margin rules every Indian trader should know. Let’s get started!

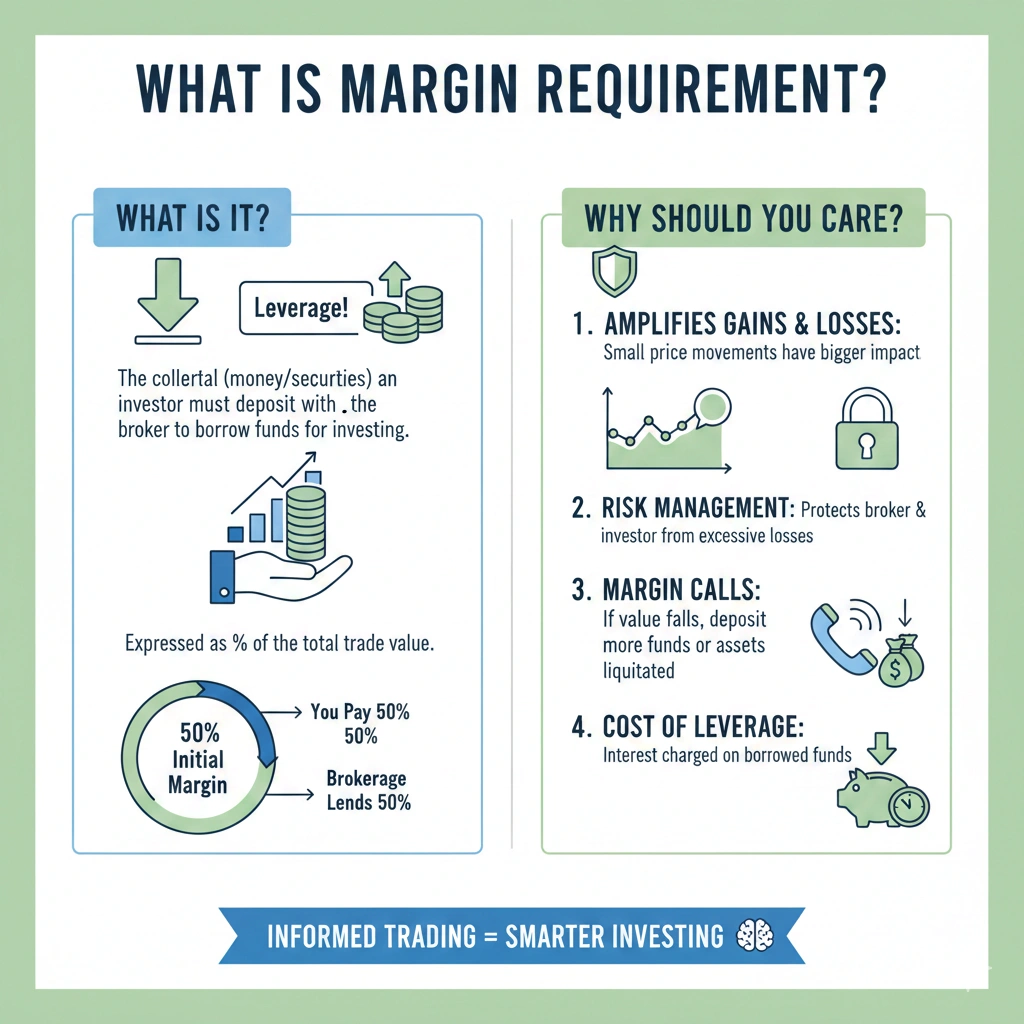

What is Margin Requirement?

Margin requirement is the minimum capital needed to open or hold a leveraged trade. For Indian F&O traders, it consists of SPAN margin + Exposure margin + ELM. For one lot of Nifty futures (75 units at ~₹24,000), the total margin required is approximately ₹2.2–₹2.7 lakh (12–15% of contract value of ~₹18 lakh).

What Is the Difference Between SPAN Margin and Exposure Margin?

If you’re trading in the F&O segment, you’ll notice your broker charges two separate margin components before you can take any position. These are SPAN margin and Exposure margin — and together they form your complete Initial Margin requirement. Understanding both is central to this margin requirement guide.

What Is SPAN Margin?

SPAN margin (Standard Portfolio Analysis of Risk) is the minimum margin amount you must maintain when trading futures and options contracts. It is a risk-based margining system used by exchanges like NSE and BSE, originally developed by the Chicago Mercantile Exchange.

SPAN margin is set equal to the single largest worst-case loss identified across all market scenarios. It is designed to cover 99% of potential single-day losses, making the entire market safer. ICICI Direct

How SPAN Calculates Your Risk — The 16 Scenario System

SPAN scans 16 different scenarios of underlying market price and volatility changes and selects the largest loss from among these 16 observations. Two of these scenarios (scenarios 15 and 16) specifically reflect extreme underlying price movements — currently defined as double the maximum price scan range. However, because such price changes are rare, the system only covers 35% of the resulting losses from these extreme scenarios.

In simple terms:

- SPAN scans price moving up, down, and sideways across 3 intervals

- At each point, it also checks volatility moving up and down

- It picks the single biggest loss from all these combinations

- That figure becomes your SPAN margin requirement

SPAN margin is recalculated daily based on price volatility and changes in your position. Since it reflects the actual risk in a position, SPAN margin varies from one instrument to another and depends on portfolio composition.

Key fact: Among Indian exchanges, Nifty SPAN margin and other index margins are evaluated six times during a trading day — so the figure you see in the morning may differ from what you see at 2 PM.

What Is Exposure Margin?

Exposure margin is an additional margin levied on top of the SPAN margin to cover any losses that might occur beyond the worst-case scenario considered by SPAN. It acts as a buffer, providing extra protection against extreme market movements. The exchange (NSE) sets the exposure margin based on factors like volatility and open interest. Samco

The exposure margin is blocked over and above the SPAN margin specifically to cushion against Mark-to-Market (MTM) losses.

How much is the Exposure Margin?

As per NSE’s official margin framework:

- For Index options and Index futures contracts: Exposure margin is 3% of the notional value of the contract. For individual stock futures and options: it is the higher of 5% or 1.5 standard deviations of the notional value of the gross open position.

SPAN vs. Exposure Margin — Quick Comparison

| SPAN Margin | Exposure Margin | |

|---|---|---|

| Purpose | Covers worst-case single-day loss | Buffer for extreme/unpredictable moves |

| Set by | NSE Clearing (exchange-level) | SEBI-mandated, collected by broker |

| Calculation | 16-scenario risk algorithm | % of notional contract value |

| For Index F&O | Dynamic, volatility-based | 3% of contract value |

| For Stock F&O | Dynamic, volatility-based | Higher of 5% or 1.5 SD |

| Changes | Updated 6x per trading day | Relatively stable, changes with policy |

The Master Formula

Total Margin (Initial Margin) = SPAN Margin + Exposure Margin

Real Example — Nifty Futures:

Assume Nifty is at ₹24,000. One lot = 75 units. Contract value = ₹18,00,000.

- SPAN Margin (~12–13% of contract value) = approx. ₹2,16,000 – ₹2,34,000

- Exposure Margin (3% of contract value) = ₹54,000

- Total Margin Required = approx. ₹2.7 – ₹2.9 lakh

These are indicative figures. Always check your broker’s SPAN margin calculator for real-time values before placing any trade.

Why Margin Matters

- Leverage: With the help of Margin you can control a larger position than your actual capital’s capacity. For example, with just ₹1.5 lakh, you might be able to trade ₹10 lakh worth of stocks or futures.

- Risk Management: SEBI sets the rules and regulations regarding Margin requirements to protect traders from excessive risk. And when your account does not have sufficient margin, you’ll get a margin call, and you’ll need to deposit more funds or either end your trade there.

- Market Stability: The main purpose behind setting margin requirements by the regulators, is to prevent market crashes caused by over-leveraged traders.

Types of Margin Requirements

- Initial Margin: The amount you need to deposit to open a position.

- Maintenance Margin: You must maintain a minimum balance in your account to maintain your position. If your account balance drops below it, you’ll get a margin call.

For Indian traders, understanding these concepts is crucial, especially with the recent changes in SEBI’s margin rules for index derivatives, a key focus of this margin requirement guide.

Why Does This Split Matter for You as a Trader?

1. Hedged positions reduce SPAN, not Exposure When you hold a hedged portfolio (e.g., a bull call spread), your SPAN margin drops significantly because the exchange recognizes reduced net portfolio risk. However, exposure margin may still be charged on the gross position in some cases.

2. SPAN changes intraday — Exposure mostly doesn’t If market volatility spikes mid-session (e.g., during an RBI announcement or budget), your SPAN margin can increase immediately — sometimes triggering a margin shortfall even if you haven’t changed your position. Always keep a 15–20% buffer above minimum margin.

3. Selling options costs significantly more than buying For option buyers, only the premium is blocked — no SPAN or Exposure margin is required. For option sellers (writers), full SPAN + Exposure margin is blocked upfront, which can be ₹1.5–3 lakh per lot depending on the instrument and volatility.

SPAN margin covers your worst-case single-day portfolio loss calculated across 16 market scenarios. Exposure margin is an additional 3% of contract value (for index derivatives) charged as a safety buffer. Together they form your total initial margin requirement = SPAN + Exposure.

Margin Per Lot Explained: How It Works

Now, let’s see what is “margin per lot”? If you’re involved in futures or options trading, then you must have heard about “lots.” In a lot there is a limited quantity decided for any financial instrument that you can buy. For example, if you buy one lot of Nifty futures you will get 75 units, while in one lot of Bank Nifty futures you will get 35 units.

How Margin Per Lot Is Calculated

The margin per lot refers to the amount of margin you will need to trade one lot of any financial instrument. To calculate the margin you need the lot size, the current price of the asset you’re trading, and the margin percentage that the exchange decides.

Here’s a simple formula:

Margin per lot = Lot size × Price per unit × Margin percentage

For example, if you want to trade one lot of Nifty futures (lot size = 75), and the current price is ₹20,000, with a margin percentage of 10%, the margin per lot would be:

75 × ₹20,000 × 10% = ₹1,50,000

So, you’d need ₹1.5 lakh to trade one lot of Nifty futures.

Why Margin Per Lot Matters

- Position Sizing: Knowing the margin per lot helps you decide how many lots you can trade with your available capital.

- Risk Management: It helps you avoid over-leveraging and getting margin calls.

- Cost Efficiency: Understanding margin per lot can help you optimize your trading strategy and reduce unnecessary costs.

For Indian traders, it’s important to keep an eye on the margin per lot for different indices and stocks, as these can change based on market volatility and regulatory updates.

What Is Extreme Loss Margin (ELM)?

When you open a derivatives position, your broker collects SPAN + Exposure margin. But there’s a third layer that many traders miss — Extreme Loss Margin (ELM). It’s the margin that covers losses SPAN simply cannot predict.

What ELM Covers

Extreme Loss Margin (ELM) is an additional margin charged by exchanges beyond normal margin requirements. It covers losses that may exceed predictions from VAR (Value at Risk) models — essentially, the “black swan” moves that standard risk models don’t account for.

Think of it this way:

- SPAN margin = covers 99% of normal market risk

- ELM = covers the remaining 1% extreme tail-risk scenarios

Who Pays ELM — Buyers or Sellers?

This is the most misunderstood part. No ELM is levied on long (buying) positions — there cannot be any offset provided since ELM is applicable only for short (selling) positions.

Option buyer: No ELM. You only pay the premium. Option seller/writer: Full ELM applies on your short position.

ELM Rates — Index vs. Stock Derivatives

For index derivatives, ELM is 2% of the notional contract value. For stock derivatives, it is 3.5% of the notional contract value. Swastika

| Segment | ELM Rate |

|---|---|

| Index Futures & Options (short) | 2% of contract value |

| Stock Futures & Options (short) | 3.5% of contract value |

| Long (buying) positions | NIL |

The Expiry Day Rule — Where ELM Gets Doubled

This is the critical update every short options seller must know.

An additional ELM of 2% is levied on short index options contracts on the day of expiry to cover potential risks due to increased volatility. Samco

This effectively raises ELM from 2% to 4% on expiry day, and the overall margin requirement increases from approximately 11% to 13% for ATM (at-the-money) contracts. SEBI

Expiry Day ELM — At a Glance:

| Day | ELM for Short Index Options | Total Approx. Margin |

|---|---|---|

| Normal trading day | 2% of contract value | ~11% of contract value |

| Expiry day | 4% of contract value (2% base + 2% additional) | ~13% of contract value |

This additional expiry day margin of 2% applies to all open short index options at the start of the day, as well as short index options contracts initiated during the day that are due for expiry on that day.

Real Example — Nifty Short Option on Expiry Day

Nifty at ₹24,000 | Lot size = 75 units | Contract value = ₹18,00,000

| Margin Component | Rate | Amount |

|---|---|---|

| SPAN Margin | ~9% | ₹1,62,000 |

| Exposure Margin | 3% | ₹54,000 |

| ELM (Normal day) | 2% | ₹36,000 |

| Total — Normal Day | ~14% | ~₹2,52,000 |

| Additional ELM (Expiry day) | +2% | +₹36,000 |

| Total — Expiry Day | ~16% | ~₹2,88,000 |

Always verify exact figures using your broker’s live margin calculator before trading.

Calendar Spread & ELM — Special Rule

For calendar spread positions in futures contracts, ELM is levied on one-third of the value of the open position of the far month futures contract — not the full position value. This benefit, however, is not available for options contracts.

Key Takeaway for Traders

If you sell (write) options — especially near expiry — always account for the additional 2% ELM in your margin planning. Failing to do so is one of the most common reasons traders face unexpected margin calls on expiry day.

Current Index Derivative Lot Sizes & Margin Requirements

Before placing any index derivative trade, you must know the exact lot size and the margin it demands. Here’s the most important update every Indian trader needs right now.

Latest Lot Size Revision — Effective January 2026

NSE revised the market lot sizes of key index derivative contracts effective from the January 2026 series, after expiry of December 2025 contracts. The changes aim to align lot sizes with current trading volumes and enhance risk management efficiency across the derivative segment.

Revised lot sizes: Nifty 50 reduced from 75 → 65 units; Bank Nifty reduced from 35 → 30 units; Nifty Financial Services reduced from 65 → 60 units; Nifty Midcap Select reduced from 140 → 120 units. Nifty Next 50 remains unchanged at 25 units.

On BSE: BSE Sensex lot size was increased from 10 → 20 units, and BSE Bankex was increased from 15 → 30 units, following BSE circulars issued in October 2024.

Updated Index Margin Table (January 2026)

| Index | Exchange | Lot Size | Approx. Contract Value | Approx. Margin Required |

|---|---|---|---|---|

| Nifty 50 | NSE | 65 units | ~₹15.5–16.5 lakh | ₹2.0–₹2.5 lakh |

| Bank Nifty | NSE | 30 units | ~₹14–15 lakh | ₹1.8–₹2.2 lakh |

| Nifty Fin Services | NSE | 60 units | ~₹12–13 lakh | ₹1.5–₹1.9 lakh |

| Nifty Midcap Select | NSE | 120 units | ~₹13–14 lakh | ₹1.6–₹2.0 lakh |

| Nifty Next 50 | NSE | 25 units | ~₹14–16 lakh | ₹1.8–₹2.2 lakh |

| BSE Sensex | BSE | 20 units | ~₹15–16 lakh | ₹1.8–₹2.3 lakh |

| BSE Bankex | BSE | 30 units | ~₹14–15 lakh | ₹1.7–₹2.2 lakh |

Margins are dynamic — always verify real-time figures using your broker’s SPAN margin calculator before placing any trade.

Why Were Lot Sizes Revised?

This revision stems from a periodic SEBI-mandated review which aims to keep the notional value of derivative contracts within a reasonable range. Since each contract now represents fewer units, traders need to recalibrate margin requirements, profit/loss estimates, and position sizing.

The key impact: the reduction in lot sizes directly reduces the margin required per contract, improving participation and making positioning easier for retail traders.

How to Use This Table Correctly

Step 1 — Find your index and current lot size Use the table above. Note that Nifty 50’s lot size is now 65, not 75 — a common outdated figure still circulating online.

Step 2 — Calculate approximate contract value

Contract Value = Lot Size × Current Index Level Example: Nifty at ₹24,000 → 65 × ₹24,000 = ₹15,60,000

Step 3 — Estimate margin

Approximate Margin = Contract Value × 13–16% (SPAN + Exposure + ELM combined) Example: ₹15,60,000 × 14% = ~₹2,18,400

Step 4 — Verify on a live calculator Use tools like Zerodha Margin Calculator, Angel One Margin Calculator, or NSE’s official margin tool for exact real-time values before entering any trade.

SEBI’s Minimum Contract Value Rule

As per SEBI mandates, the contract value (Index Points × Lot Size) of all F&O contracts must remain between ₹5–10 lakh. If the contract value of any index moves beyond this range due to index level changes, an upward or downward revision in lot size is carried out in the periodic review.

This is why lot sizes change periodically — it’s not arbitrary. As indices rise, lot sizes are reduced to keep contracts accessible. As indices fall, lot sizes may be increased to maintain minimum notional value.

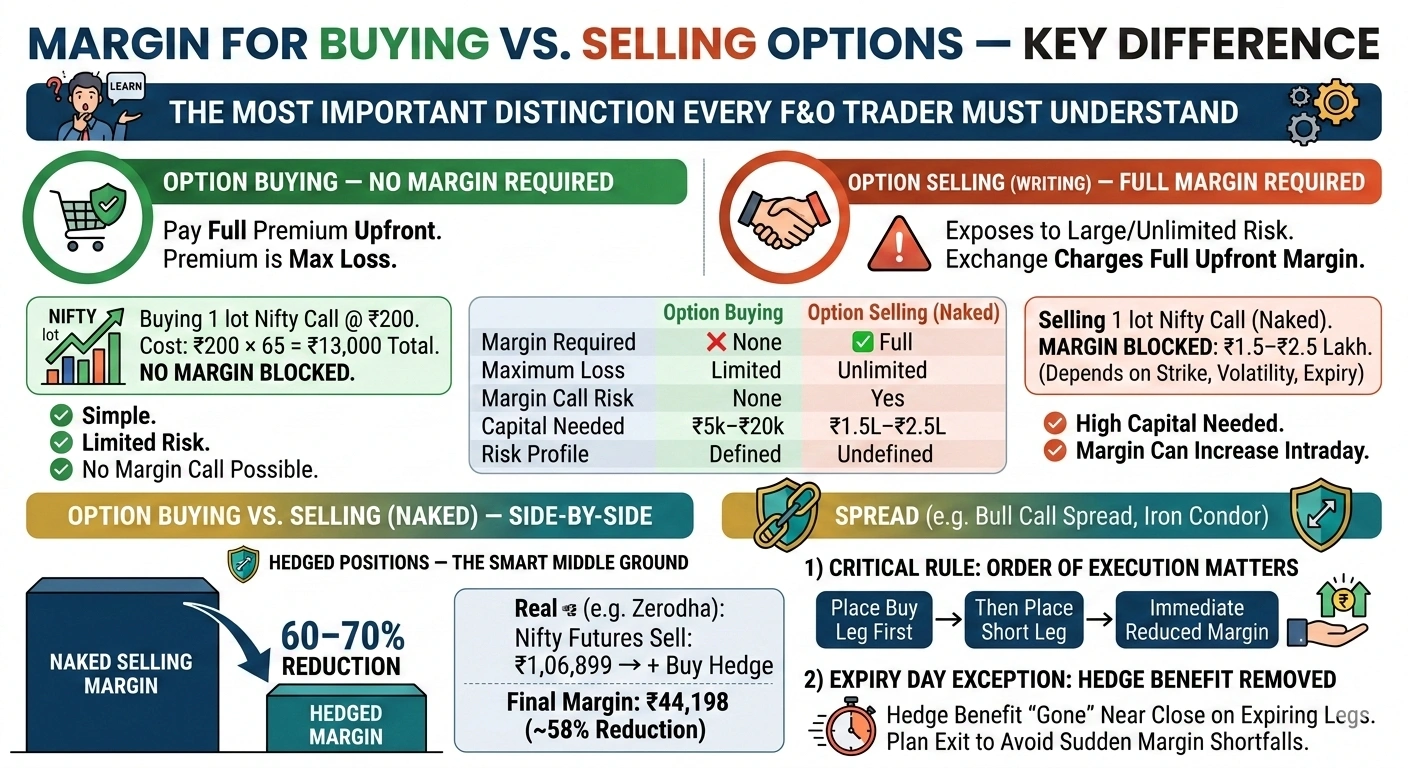

Margin for Buying vs. Selling Options — Key Difference

This is the most important distinction every F&O trader must understand before entering the market. Your option buying margin and option selling margin are completely different — and confusing them is one of the most common beginner mistakes.

Option Buying — No Margin Required

If you buy a Call or Put option, you do not need to post any margin. You simply pay the full premium upfront, and that premium itself is your maximum possible loss — nothing more can be taken from your account.

Example:

Buying 1 lot of Nifty Call at ₹200 premium Cost = ₹200 × 65 units = ₹13,000 total No additional margin blocked. Maximum loss = ₹13,000.

Simple. Limited risk. No margin call possible.

Option Selling (Writing) — Full Margin Required

Selling options exposes you to unlimited risk (for naked calls) or large risk (for naked puts). The exchange therefore charges full upfront margin — comprising SPAN + Exposure + ELM — before allowing you to take any short position.

Example:

Selling 1 lot of Nifty Call (naked) Margin blocked = ₹1.5–₹2.5 lakh depending on strike, volatility, and expiry proximity

High capital requirement. Margin can increase intraday if volatility rises.

Option Buying vs. Selling — Side-by-Side

| Option Buying | Option Selling (Naked) | |

|---|---|---|

| Margin Required | ❌ None — premium only | ✅ Full SPAN + Exposure + ELM |

| Maximum Loss | Limited to premium paid | Potentially unlimited (naked calls) |

| Margin Call Risk | None | Yes — if market moves against you |

| Capital Needed (Nifty, 1 lot) | ₹5,000–₹20,000 (premium) | ₹1.5–₹2.5 lakh |

| Risk Profile | Defined risk | Undefined / high risk |

Hedged Positions (Spreads) — The Smart Middle Ground

When you pair a short option with a long option to create a hedged spread, margin requirements drop by approximately 60–70% compared to a naked selling position. A spread that previously needed ₹1 lakh may only need around ₹30,000 after the hedge benefit is applied.

Bull call spreads, bear put spreads, iron condors, and straddles with hedges are all considered margin-efficient strategies under current SEBI rules. By limiting maximum loss potential, these defined-risk trades qualify for significantly reduced margins.

Real Example from Zerodha data: An unhedged Nifty futures sell position requires approximately ₹1,06,899 in margin. After adding a buy hedge, the final margin drops to ₹44,198 — a reduction of over 58%.

One Critical Rule — Order of Execution Matters

If you sell (short) options or execute futures first, the system demands full margin until you place the hedge. However, if you place the buy (long) option order first before the short leg, the system immediately recognizes the hedge and blocks the lower hedged margin from the start.

Pro tip: Always enter your long (buy) leg first, then the short leg — to immediately benefit from reduced hedged spread margin and avoid locking up excess capital.

Expiry Day Exception — Hedge Benefit Removed

On expiry day, if you hold a hedged position where one leg is expiring, the exchange removes the margin benefit for that expiring leg. The hedge is considered “gone” near close, and brokers may ask for full margin or auto-square off the position.

Always plan your exit or rollover before expiry day to avoid sudden margin shortfalls on hedged positions.

Option buyers pay only the premium — no margin required. Option sellers must pay full SPAN + Exposure + ELM margin (₹1.5–₹2.5 lakh per Nifty lot). Using hedged spread strategies like a bull call spread reduces this margin by 60–70%, making them the most capital-efficient way to sell options.

Index Margin Rules for Indian Traders: What’s Changed?

In recent years, SEBI (Securities and Exchange Board of India) has introduced several changes to margin rules for index derivatives. These changes are designed to protect retail traders from excessive risk and ensure market stability.

Key Changes in SEBI’s Margin Rules

- Contract Sizes: As per the latest news the SEBI has introduced a standardized design for index derivatives, the lot size has been decreased. For example, the lot size for nifty futures has been decreased from 75 to 50 units.

- Upfront Margin: As per the new rules the traders need to pay the full margin ahead of time before taking a position, rather than paying it later.

- SPAN Margin and Exposure Margin: SEBI has introduced SPAN (Standard Portfolio Analysis of Risk) margin and exposure margin for index derivatives. SPAN margin is calculated based on the potential risk of the portfolio, while exposure margin is an additional buffer to cover extreme market movements.

Impact on Indian Traders

- Higher Capital Requirement: Due to these new changes the traders will need to have more capital to trade index derivatives.

- Reduced Leverage: Now it will become a little difficult for traders to trade larger positions with small amounts of capital.

- Better Risk Management: It might sound restrictive now, but the only reason behind this is to protect traders from excessive risk and potential losses.

Example Calculation

Let’s say you want to trade one lot of Nifty futures after the recent changes. The lot size is now 50 units, and the current price is ₹30,000. If the margin percentage is 10%, the margin per lot would be:

50 × ₹30,000 × 10% = ₹1,50,000

So, you’d need ₹1.5 lakh to trade one lot of Nifty futures, compared to ₹1 lakh before the changes.

Factors Affecting Margin Requirements

Several factors can affect margin requirements for trading in India. Understanding these factors is a critical component of any margin requirement guide that can help you manage your risk and avoid margin calls.

Security Type

- Stocks: In the case of stocks the margin requirement is lower as compared to futures and options.

- Futures and Options: This section of trading is highly volatile which leads to high margin requirements.

- Indices: The Index derivatives follow their own margin rules, which change according to market conditions and regulatory updates.

Market Volatility

- High Volatility: The margin requirements increase during the highly volatile market to protect you from potential losses.

- Low Volatility: When the market is stable the margin requirement can be low.

Brokerage Policies

- Broker-Specific Rules: Different brokerage houses have their own margin rules, which means the margin you need may vary from broker to broker.

- Regulatory Requirements: Even though SEBI and other regulators have set a limit of minimum margin required, brokers can still set their own requirements if they choose.

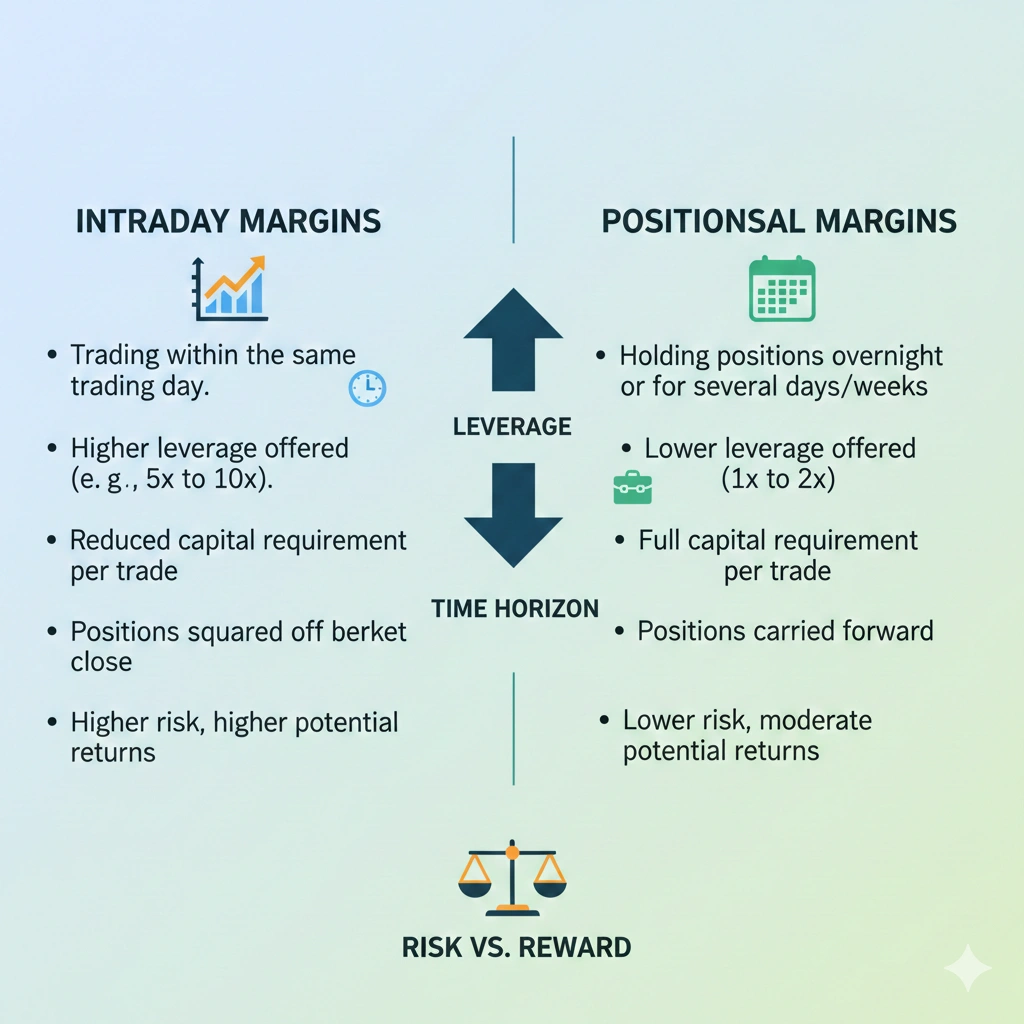

Intraday vs Positional Margins

- Intraday Margins: The margin for intraday trades is lower in comparison to positional margin because it ends within the same day.

- Positional Margins: The positional margins are higher because they are held overnight, and are more risky.

What Is a Margin Call and How to Avoid It?

A margin call is triggered when your account balance falls below the maintenance margin level. Your broker will either:

- Ask you to deposit additional funds immediately, or

- Forcefully square off your position (auto-square-off)

How to avoid a margin call:

- Keep a 20–30% buffer above the minimum margin requirement

- Use stop-loss orders to cap losses before they erode margin

- Avoid trading all your capital — keep free margin available at all times

- During high-volatility events (budget, RBI policy, elections), margins can spike — pre-check with a margin calculator

How to Calculate and Manage Margin Effectively

As a trader you must know basic calculations related to margin. Here’s a step-by-step margin requirement guide:

Step-by-Step Guide to Calculating Margin

- Determine the Lot Size: Check the given lot size of the instrument you want to trade.

- Find the Current Price: Look up the current price of the underlying asset.

- Check the Margin Percentage: Find out the margin percentage set by the exchange or your broker.

- Calculate Margin per Lot: Here’s the formula: Lot size × Price per unit × Margin percentage.

- Add Up All Positions: If you’re trading multiple lots or instruments, add up the margin requirements for all positions.

Tools and Calculators

| Tool Name | Type | Key Feature | Usage |

| Angel One Margin Calculator | Online Calculator | Calculates SPAN + exposure margin | Quick F&O margin checks |

| Samco Margin Calculator | Online Calculator | Equity, commodity, F&O margin | Multi-segment margin estimates |

| ProStocks F&O Calculator | Online Calculator | Multi-leg strategy margin breakdown | Detailed futures & options margin |

| NSE India Margin Calculator | Official Calculator | Computes risk-based margin | Accurate equity margin requirement check |

| Tradebulls F&O Calculator | Online Calculator | Multi-leg F&O margin calculation | Complex option and futures margin estimations |

Tips for Managing Margin

- Monitor Your Account: Regularly check your account balance and margin requirements to avoid margin calls.

- Diversify Your Portfolio: It’s a basic rule of trading to never use all your capital on one single trade. Always diversify the capital to divide the risk.

- Stay Updated: stay up-to-date with margin rules as they can change on bases of market conditions and regulatory updates. Stay informed to avoid surprises.

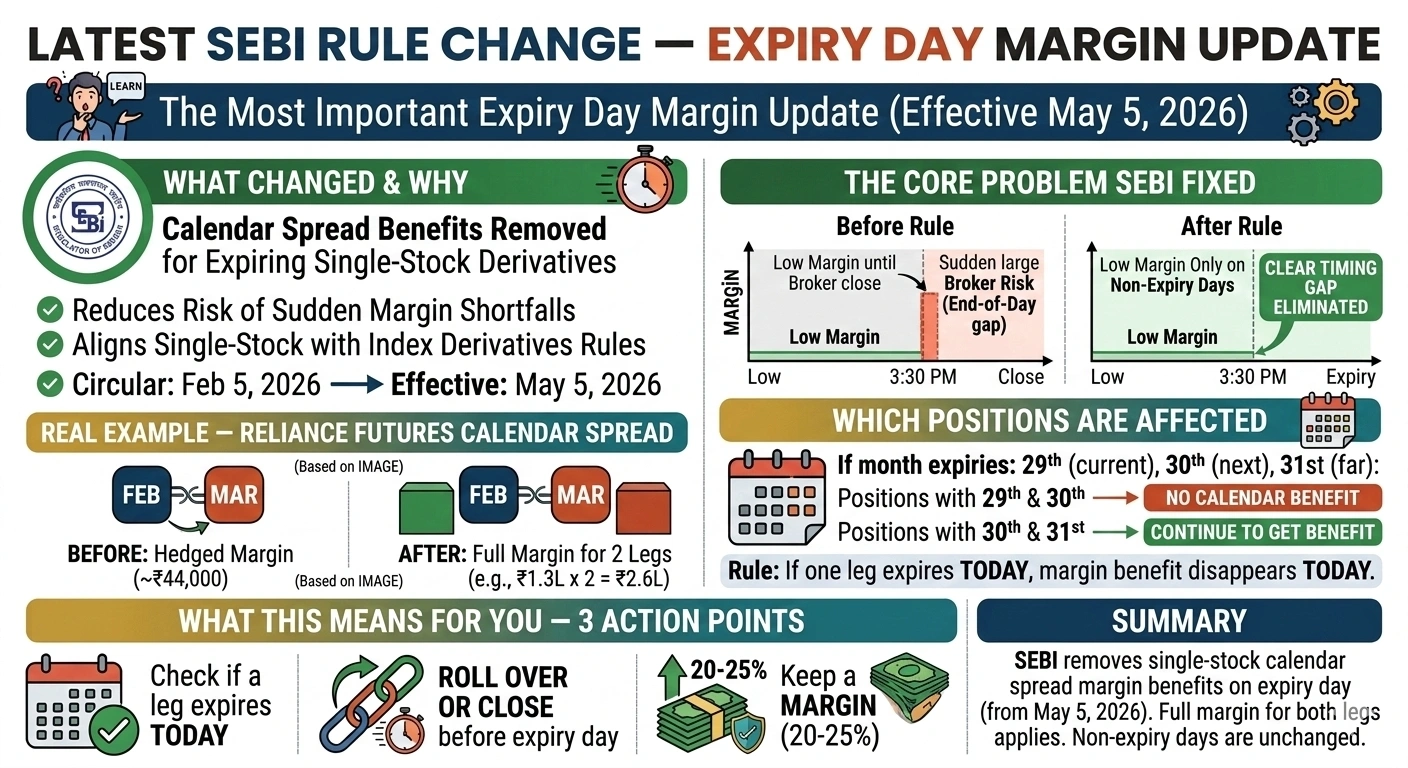

Latest SEBI Rule Change — Expiry Day Margin Update (Effective May 5, 2026)

This is the most important expiry day margin update of the year — and most traders are still unaware of it.

What Changed and Why

SEBI has announced that calendar spread margin benefits will no longer be applicable on the expiry day for contracts involving single-stock derivatives. The regulator issued a circular on February 5, 2026, following concerns raised by trading members and a review by the Secondary Market Advisory Committee (SMAC). This move is designed to reduce the risk of sudden margin shortfalls that can disrupt market stability.

Any position involving an expiring single-stock derivative contract will not be eligible for offsetting benefits during the expiry session. The effective date is May 5, 2026. The new rules will align calendar spread treatment for single-stock derivatives with that of index derivatives — and give traders enough time during market hours to bring in additional margin, roll over positions, or close trades.

The Core Problem SEBI Fixed

Under the earlier system, on expiry day, clients continued to enjoy lower calendar spread margin until 3:30 PM. After market close, one leg expired and margins rose sharply — but brokers could only ask for End-of-Day margins after markets were already shut. This timing gap increased operational and financial risk, especially during volatile conditions. The new rule eliminates this gap entirely.

Exactly Which Positions Are Affected

If monthly expiries fall on the 29th (current month), 30th (next month), and 31st (far month):

- Positions involving 29th & 30th, or 29th & 31st → will NOT get calendar spread benefits on the 29th

- Positions involving 30th & 31st → will continue to get the benefit on the 29th. The rule is simple: if one leg of your spread expires today, the margin benefit disappears today.

Real Example — Reliance Futures Calendar Spread

Consider a calendar spread in Reliance futures — buying February futures and selling March futures (1 lot each). The margin for a single futures contract is around ₹1.3 lakh per lot. Until now, the hedged spread reduced this significantly. From May 5, 2026, on the February expiry day, the spread margin benefit disappears — and you must hold full margin for both legs separately.

What Stays Unchanged

The existing margin calculations for calendar spread positions involving all expiries other than the contracts expiring on a given day remain unchanged. Non-expiring spreads continue to enjoy the full margin benefit as before.

Only expiry-day treatment changes. All other trading days — no impact.

What This Means for You — 3 Action Points

1. Always check if a leg expires today Before market open on any expiry day, check whether any leg of your single-stock derivative calendar spread is set to expire. If yes — full margin applies from the start of that session.

2. Roll over or close before expiry day The new rule is specifically designed to give clients and brokers more time to manage margin requirements or close calendar spread positions on expiry days. Use this window — don’t wait for the last hour.

3. Keep a margin buffer on expiry days Even if you’re not in a calendar spread, expiry day margin across all derivatives tends to spike. Maintain at least a 20–25% buffer above your minimum margin requirement on every expiry day.

From May 5, 2026, SEBI has removed calendar spread margin benefits for single-stock derivatives on expiry day — aligning them with existing index derivative rules. If one leg of your spread expires that day, full margin applies for both legs. Non-expiry days and non-expiring spreads are

Intraday (MIS) vs. Overnight (NRML) Margin — Which Is Right for You?

Every time you place a derivatives order, you must choose between two product types: MIS or NRML. This single choice directly impacts how much margin you need, how long you can hold your position, and your risk exposure.

What Is MIS Margin?

MIS (Margin Intraday Square-off) is used for intraday trading with leverage. It requires a lower upfront margin compared to other order types, and if not closed manually, the broker automatically squares off the position at the end of the trading day.

For Equity futures, MIS margin is 45% of the NRML margin. For Index futures, it is 35% of NRML margin. For Commodity and Currency futures, MIS margin is 50% of NRML margin.

Less capital locked. Ideal for disciplined intraday traders.

What Is NRML Margin?

NRML (Normal) requires the full initial margin — comprising SPAN + Exposure margin — as mandated by NSE/BSE. You must maintain adequate margin in your account as long as the position is open, accounting for daily Mark-to-Market (MTM) adjustments. Unlike MIS, NRML offers no additional leverage.

NRML allows traders to hold futures and options contracts until they expire — ideal for those with a longer time horizon beyond intraday trading.

Full flexibility. Hold positions for days, weeks, or until expiry.

MIS vs. NRML — Side-by-Side Comparison

| MIS (Intraday) | NRML (Positional/Overnight) | |

|---|---|---|

| Full Form | Margin Intraday Square-off | Normal Margin Order |

| Margin Required | 35–50% of NRML margin | Full SPAN + Exposure margin |

| Nifty Futures (1 lot) | ~₹70,000–₹90,000 | ~₹2.0–₹2.5 lakh |

| Position Duration | Same day only | Overnight — till expiry |

| Auto Square-off | Yes — ~3:20 PM | No (unless margin breach) |

| Leverage | Higher (lower capital needed) | No additional leverage |

| MTM Risk | None (position closes today) | Yes — daily MTM settlement |

| Best For | Intraday scalpers, day traders | Swing traders, positional traders |

The Auto Square-Off Rule — What Traders Get Wrong

From 3:20 PM to 3:25 PM, all open MIS positions in Equity and F&O are automatically squared off if not closed manually. Brokers like Zerodha charge a penalty of ₹50 per order for auto square-off.

Conversion from MIS to NRML after 3 PM is risky and often not permitted close to the cut-off. Most brokers expect conversions to be completed before 3:10 PM, after which positions are locked for auto square-off.

Broker square-off times vary — Zerodha, Angel One, Upstox, and others each have slightly different cut-off windows. Always check your broker’s specific auto square-off time before trading MIS.

Can You Convert MIS to NRML Mid-Day?

Yes — but with conditions.

If an MIS position is not squared off before the broker’s cut-off, it may get automatically converted to an NRML or CNC position and carried forward to the next day. However, the broker’s RMS desk will square off such a position the following trading day without a margin call if the required cash is not available.

Convert MIS → NRML only if you have sufficient overnight NRML margin available in your account — otherwise your position may be forcibly closed.

Which Should You Choose?

Choose MIS if:

- You’re an intraday trader and will monitor positions actively

- You want to trade with lower capital

- You’re comfortable closing all positions before 3:10 PM

Choose NRML if:

- You’re a swing or positional trader

- You want to hold beyond the same day

- You have sufficient capital to maintain full overnight position margin

MIS margin requires only 35–50% of the full margin (depending on segment) and auto-squares off at ~3:20 PM. NRML margin requires full SPAN + Exposure and lets you hold positions overnight or until expiry. For Nifty futures, MIS needs ~₹70,000–90,000 vs. NRML’s ~₹2–2.5 lakh per lot.

FAQs: Margin Requirement Guide

Q: What is the minimum capital needed to trade Nifty futures?

To trade one lot of Nifty 50 futures (75 units), you need approximately ₹2.2–₹2.7 lakh as margin, based on a contract value of ~₹18 lakh at current index levels and a 12–15% margin requirement.

Q: What is SPAN margin in simple terms?

SPAN margin is the minimum risk-based margin calculated by the exchange using 16 market scenarios to cover the worst possible single-day loss on your position.

Q: What happens on expiry day for margin?

On expiry day, ELM (Extreme Loss Margin) of 2% is applied to all short option positions. Additionally, calendar spread benefits are no longer available for contracts expiring that day — meaning margin requirements rise sharply near close.

Q: Can I reduce my margin requirement legally?

Yes — by using hedged strategies like spreads (bull call spread, bear put spread, iron condor). A hedged position’s margin can be 50–70% lower than a naked sell position because the exchange recognizes reduced net risk in your portfolio.

Final Thoughts: Build Your Trades on a Strong Margin Foundation

This margin requirement guide covers everything an Indian F&O trader needs — from the basics of SPAN margin and Exposure margin, to Extreme Loss Margin (ELM), current index lot sizes, the MIS vs NRML choice, and SEBI’s latest expiry day margin rules effective May 2026.

Margin is not just a number your broker shows you before you click “Buy.” It is the foundation of every trade you take. Get it wrong and you face margin calls, forced exits, and unexpected losses. Get it right and you trade with confidence, clarity, and full control of your risk.

Three rules to carry with you always:

- Never use 100% of your capital as margin — always keep a 20–25% buffer

- On every expiry day, check your positions early — margins spike, spread benefits disappear

- Always verify live margin figures on your broker’s SPAN margin calculator before entering any trade

Stay updated. Trade smart. And revisit this guide every time SEBI revises the rules — because in Indian markets, margin requirements are never static.

For more guides on F&O trading, risk management, and market strategy — visit InsightfulTrade.

Author: Arihant Jain

Trading Experience: 5+ Years

Arihant Jain is a financial markets analyst and trading educator with expertise in Forex, Indices, Crypto, and risk-managed trading systems. His insights are based on real trading experience, data-driven analysis, and transparent market understanding. All content is reviewed for accuracy and aligns with Google’s EEAT guidelines.

Risk Disclaimer:

Trading involves substantial risk. All information is for educational purposes only and should not be taken as financial advice. Always do your own research.

Last Updated: 5 March 2026