Forex trading is rapidly rising in India; people are using global apps and online sites for trading. But what confuses the traders is how to report the losses correctly because of the unclear forex trading rules in India. This gap between your trading and your tax filing creates real risks, even if you aren’t actually making money.

In this blog, we explain how and why you must declare these losses and help you understand the tax logic behind the rules so you can stay on the right side of the law.

Declaring Forex Losses in India – Snapshot Table

| Aspect | What It Means | Why It Matters |

| Loss Declaration | Reporting losses in ITR | Enables carry forward |

| Income Head | Business income (most cases) | Determines rules |

| Due Date | Timely ITR filing | Mandatory for carry forward |

| Documentation | P&L, trade records | Proof during scrutiny |

| Carry Forward | Future profit adjustment | Reduces future tax |

Understanding Forex Trading Under Indian Tax Law

Before you think about declaring Forex losses in India, you need to know how the Income Tax Act 1961 actually views your trades. Not all forex transactions are treated the same under Indian tax law; the rules change based on why you made that trade.

Common Forex Transaction Categories

- Trading for profit (like derivatives or margin trading)

- Forex contracts for business hedging

- Currency exchange for business and travel.

This distinction is important because treatment for losses and carry forward trading losses rules are vastly different.

Why Declaring Forex Losses in India Is Mandatory

A common myth is that you don’t need to report your losses while computing your taxable income. But in reality, it’s considered to be essential in India to report losses, even if:

- No tax is payable

- Net income falls below taxable limits

- Losses exceed gains

Why the Income Tax Department Requires Disclosure

- Loss validation

If you want to claim losses, you need to report them in your official return. - Carry forward eligibility

Unregistered losses can’t be carried forward to next year’s taxes. - Audit and scrutiny alignment

Banks and brokers already report your activity, so it is better to be honest.

Skipping this can hurt your credibility and ruin your future tax-saving chances.

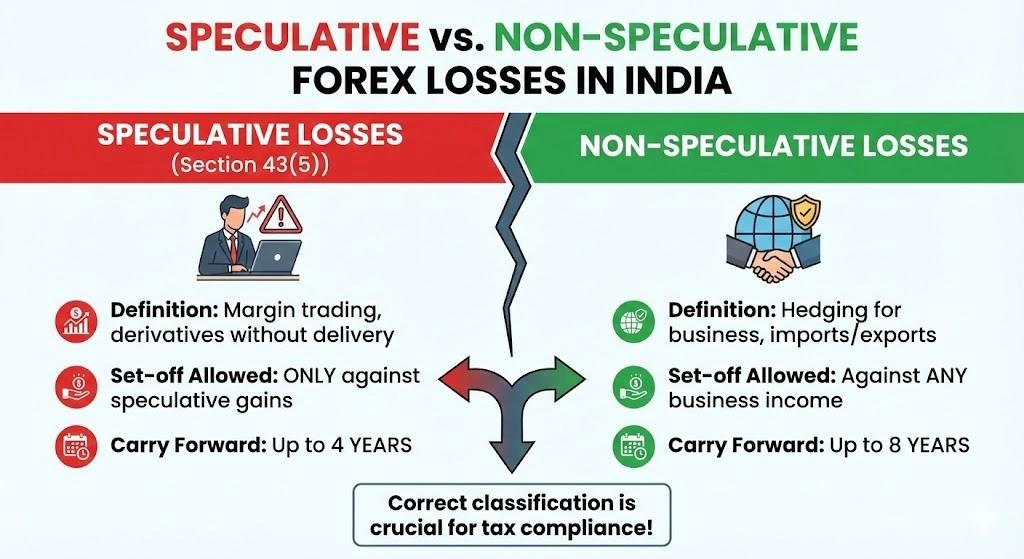

Speculative vs Non-Speculative Forex Losses

The most important part of declaring Forex losses in India is knowing if the loss is speculative or not.

Speculative Forex Losses

As per section 43(5) of the Income Tax Act, if you are trading on margin or using derivatives without taking actual delivery, it is usually considered as speculative.

Tax Impact

- You can use it to cancel out others’ speculative gains

- And it can be carried forward for 4 years.

Non-Speculative Forex Losses

Forex losses are seen as non-speculative if they happen while protecting a real business or relate to imports, exports, and overseas operations.

Tax Impact

- You can use them to set off against business income

- And carry them forward for up to 8 years.

This classification is why getting the label right matters just as much as the actual reporting.

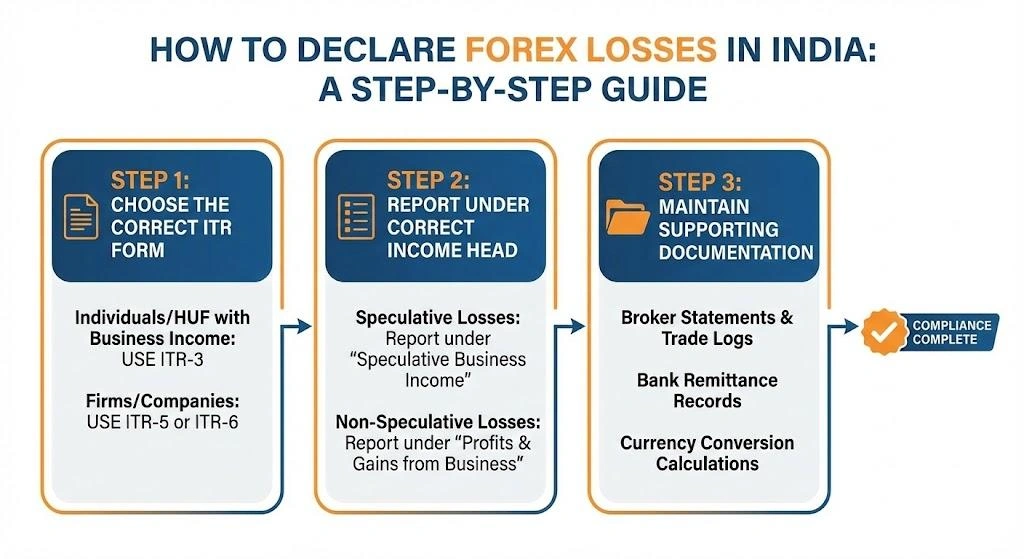

How to Declare Forex Losses in India

Step 1: Choose the Correct ITR Form

- ITR-3: This one is for Individuals or HUFs with business income

- ITR-5/6: For the Firms or companies

Forex trading is treated as business income, so simple return forms like ITR-1 or ITR-2 won’t work.

Step 2: Report Under Correct Income Head

- Speculative: list under speculative business income

- Non-speculative: list under profits and gains from business

This step determines whether your loss can be carried forward.

Step 3: Maintain Supporting Documentation

To report forex losses in India, you need to keep:

- Broker statements and trade logs

- Bank remittance records

- Currency conversion calculations

Good paperwork builds your credibility and protects you if the tax officer ever asks a question.

Carry Forward Trading Losses: Rules Explained

Understanding carryforward trading losses is essential for long-term tax planning.

Key Rules

| Loss Type | Carry Forward Period | Set-off Allowed Against |

| Speculative Forex Loss | 4 years | Speculative gains only |

| Non-Speculative Forex Loss | 8 years | Business income |

Important Compliance Condition

As per section 139(1), you can only carry forward losses if the return is filed within the due date. That’s why it’s important to declare forex losses in India on time, even during a loss-only year.

For example, suppose you incurred a speculative forex loss of ₹200,000 in the financial year 2025–26. If you file your income tax return within the due date, that loss does not disappear. However, it cannot be adjusted against regular business income or salary. It can only be set off against speculative gains.

You are allowed to carry this loss forward for four assessment years. That means you can use it to reduce speculative profits earned up to FY 2029–30. If you do not have any speculative gains within that period, the unadjusted loss will lapse after that.

Common Mistakes While Declaring Forex Losses in India

- Completely ignoring your losses

- Picking the wrong tax type

- Making mistake while recording speculative trades

- Missing the last date of tax filing

- Thinking foreign brokers have no home tax

Any of these errors can stop you from using your current losses to reduce your taxable income, costing you money for years.

Compliance Perspective: Why Accuracy Matters

From a legal perspective, saving taxes is not the only reason behind declaring forex losses in India; it also helps with.

- Keeping your financial story clear

- Staying in the line with foreign exchange rules

- Lowering the risk of audit

- Planning for future profits

Tax officials now use a data-matching system to compare your filing with banks’ and brokers’ records. Declaring forex losses in India ensures everything adds up and keeps you off their radar.

Tools and Platforms That Simplify Forex Loss Reporting

The current tax tracking tools make things easy for you:

- They differentiate speculative and regular trades for you

- They handle tricky currency conversation automatically

- They keep the track of your losses time

These tools will help in preventing manual mistakes and ensure you’re ready for a tax audit.

Conclusion

Declaring forex losses in India is your legal duty; you don’t have the option to ignore it. And it can directly affect your taxable income, so ensure that you’re reporting it correctly. Mastering the speculative rules, hitting filing deadlines, and keeping solid records are key to staying safe.

If you want further information or guidance with active trading and tax rules, connect with InsightfulTrade. They help traders maintain their legal duties while trading to avoid any trouble with the regulators.

FAQs: Declaring Forex Losses in India

1. Is declaring forex losses in India mandatory even if I have no income?

Yes. Declaring forex losses in India is required if you want to claim or carry forward those losses.

2. Can forex losses be adjusted against salary income?

Only non-speculative business-related forex losses may be adjusted. Speculative losses cannot.

3. Do Indian tax rules apply to foreign forex brokers?

Yes. Indian residents must comply with Indian tax laws regardless of broker location.

4. Are there tools to help with forex tax compliance in India?

Yes. Several tax platforms and analytics tools, including compliance-focused solutions, help track and report forex losses accurately.

Author: Kumkum Chandak

Experience: 3+ Years in Trading Research & Market Content Strategy

Kumkum Chandak is a trading content strategist and market research writer who specializes in simplifying technical analysis, trading tools, and strategy-driven educational content. Her work is optimized for EEAT, accuracy, and user intent, ensuring every article delivers practical insights for traders of all levels.

Risk Disclaimer:

All content is strictly educational and not financial advice. Trading involves substantial risk. Always perform your own analysis or consult a professional advisor.

Last Updated: 6 February 2026