Quick Summary

Forex income reporting in India is one of the most misunderstood parts of trading. Even though there are strict limits over how you trade the forex market, the money you earn is still something that the tax office expects you to report. Many traders wrongly assume that using a broker from abroad, making small gains, or lacking clarity in rules means they can skip the paperwork. The truth is, Indian tax law cares about where you live and the fact that you earned money, regardless of platform. In this blog, we’ll learn how to report your income properly, why taxes still apply in grey areas, and why keeping a solid record is important to stay compliant.

Snapshot Overview

| Aspect | Position in India |

| Retail forex legality | Restricted |

| Tax on forex income | Applicable |

| Offshore trading income | Reportable |

| Income classification | Business or other income |

| Documentation importance | Very high |

The Core Problem: Why Forex Income Reporting in India Is Confusing

One question that confuses a lot of traders is this: “If forex trading is restricted, why do I have to pay tax on it?”

This mindset causes widespread non-compliance in forex income reporting in India.

The confusion happens because:

- The RBI decides which financial instrument you can exchange

- The Income Tax Act establishes rules for all the income you earn

- These laws operate independently

As a result, even when trading legality is unclear, trading tax India rules can still apply.

Why Trading Restrictions Do Not Cancel Tax Obligations

It’s important to know why you still have to pay tax.

1. Income Tax Law Don’t Care Where the Money Came From

Indian tax law taxes income based on:

- Your residency

- The type of income

- When you received it

2. This Happens With Other Income Too

Similar reasoning can be used for:

- Freelancing for foreign clients

- Crypto income (before formal regulation)

- Informal business income

This same logic applies to forex income reporting in India.

What Counts as Forex Income?

Forex traders need to identify which type of earnings is considered as taxable income to correctly report their profits.

Common Forex Income Sources

- Profits from currency trading

- Gains from leveraged forex positions

- Net trading surplus after expenses

The main factor to evaluate is net income because it surpasses the combined total of all trading activities.

How Forex Income Is Classified for Tax Purposes

There is no “forex income” category under Indian tax law. Instead, it’s all about your trading behavior.

1. Business Income (Most Common)

Applied when trading is

- Frequent

- Systematic

- Profit-oriented

Most active traders fall into this category.

2. Income from Other Sources

Applied when:

- Trading is occasional

- Volumes are small

- It’s not a regular activity

Tax officers look at frequency and goals.

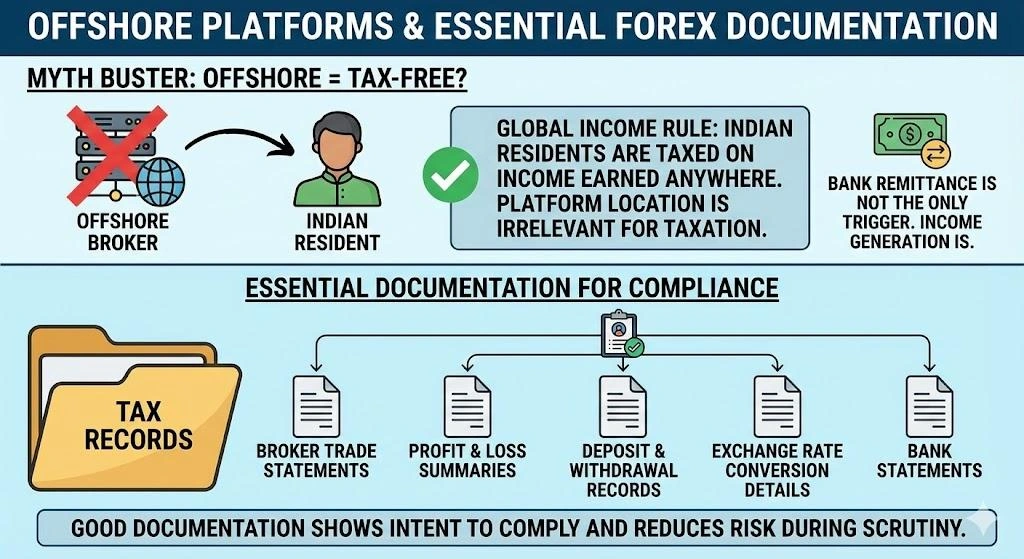

Offshore Forex Platforms and Indian Tax Reporting

Many traders think that using offshore brokers will exempt them from paying tax. This is incorrect.

Why Offshore Income Is Still Taxable

- Indian residents are taxed on their worldwide earnings

- The platform’s location doesn’t change your tax duty

- Tax is triggered when you profit, not just when you withdraw

Thus, offshore profits must still be reported when you declare forex income.

Role of Banks in Forex Income Scrutiny

Banks act as financial guardians instead of tax collectors, but they maintain control over who can access their services.

What Banks Monitor

- Large sums of money coming in

- Frequent transfers from abroad

- Inconsistent transaction narratives

The unclear explanation will trigger account reviews, which will create new future tax problems.

Documentation: The Backbone of Forex Income Reporting in India

Due to lack of clarity in the rules, your paperwork becomes the most important source of self-defense.

Essential Records to Maintain

- Broker trade statements

- Profit and loss summaries

- Deposit and withdrawal records

- Exchange rate conversion details

- Bank statements

These records are the proof of your good faith, which is crucial if you’re ever questioned.

How to Declare Forex Income in India

Because of uncertainty regarding forex income tax, traders use standard reporting methods.

Common Reporting Method

- List income in the right part of your ITR

- Include how you calculate your profit

- Maintain supporting records

This approach follows the safe, standard way of handling trading tax in India.

Why Non-Reporting Is Riskier Than Over-Reporting

The fear of regulatory scrutiny leads traders to avoid reporting their activities. In reality:

The Risks of Hiding

- Notices for unknown source of income

- Penalties for hidden earnings

- Trouble explaining bank deposits later

Tax authorities focus on maintaining consistency rather than achieving absolute perfection in their operations.

India vs Other Jurisdictions: Why India Is Stricter

India’s forex law is much more cautious than any other nation’s

Reasons

- Strict control on capital flow

- Keeping the rupee stable

- Preventing misuse of money channels

This explains why forex income reporting in India is enforced even when trading legality is restricted.

Compliance Red Flags to Avoid

To stay on the right side of forex income reporting in India, avoid:

- Managing money for other people

- Earning referral commissions

- Acting as an introducing broker

- Using your account for group trading

These moves change how your income is viewed and attract extra attention.

Why Clear Forex Tax Guidance Is Still Missing

In India forex is regulated by the RBI, while the CBDT handles taxes. This split leads to:

- Delayed rules

- Case-by-case assessments

- Reliance on general principles

Until they sync up better, traders need to stay cautious.

A Practical Compliance Mindset

Here’s what you can do to stay on the right side of the law:

- Be honest about your earnings

- Play it safe with your income labels

- Keep your paperwork organized

- Stay consistent year after year

This is the best way to handle Indian tax authorities.

Conclusion

Forex income reporting in India isn’t optional, even if the trading rules are not clear yet. The tax law requires you to report all your profits, whether from local activities or foreign operations, because your tax obligations depend on your residence and the source of your earnings. Traders who follow a cautious approach by declaring the gains and keeping detailed paperwork will find it much easier to stay out of trouble. Staying honest and transparent is your best strategy in forex trading.

To stay updated with the current tax trends and global rules, connect with InsightfulTrade. They provide excellent analysis tailored specially for Indian traders.

FAQs: Forex Income Reporting in India

1. Is forex income taxable in India?

Yes. Any money you make from forex can be taxed, though how it’s labeled might change.

2. Do I need to declare forex income from offshore brokers?

Yes. Indian residents are taxed on global income.

3. Are tools like MT4 or MT5 taxable?

No. You aren’t taxed for using software, only on the actual profit you earned with it.

4. How is forex income usually classified?

Most active traders report it as business income under trading tax India rules.

Author: Kumkum Chandak

Experience: 3+ Years in Trading Research & Market Content Strategy

Kumkum Chandak is a trading content strategist and market research writer who specializes in simplifying technical analysis, trading tools, and strategy-driven educational content. Her work is optimized for EEAT, accuracy, and user intent, ensuring every article delivers practical insights for traders of all levels.

Risk Disclaimer:

All content is strictly educational and not financial advice. Trading involves substantial risk. Always perform your own analysis or consult a professional advisor.

Last Updated: 3 February 2023