You may have earned some profits, and you may be contemplating how to withdraw money from a forex broker in India, but it is not as easy as it may seem. Because of the RBI laws, traders will be required to adhere to strict forex withdrawal laws in India, select viable forex withdrawal tools in India, and be acquainted with the charges. The following guide details the procedure, deadlines, and forex withdrawal charges in India, which will enable you to transfer finances to your bank account without risks.

Key takeaway

- Only regulated brokers should be used.

Select registered brokers under SEBI to make safe and compliant withdrawals.

- Choose the appropriate technique.

Bank transfer, UPI, e-wallets, or SWIFT—choose according to the speed and price.

- Watch withdrawal fees

Note the forex withdrawal charges in India, such as conversion and transfer charges.

- Follow legal rules

Adhere to the guidelines of RBI and FEMA and declare forex income in ITR.

Understanding the Regulatory Framework: What Indian Traders Must Know First

Prior to knowing how to withdraw money from a forex broker, comprehend Indian regulations.

The Foreign Exchange Management Act of 1999 regulates forex by the Reserve Bank of India and the Securities and Exchange Board of India. It can only be traded through SEBI brokers in the National Stock Exchange, Bombay Stock Exchange, and Metropolitan Stock Exchange of India in INR pairs.

Key points:

- Liberalized Remittance Scheme USD 250,000/year limit.

- Withdrawals made offshore can be subject to tax/scrutiny.

- SEBI brokers guarantee withdrawals that are easy and in compliance with the law.

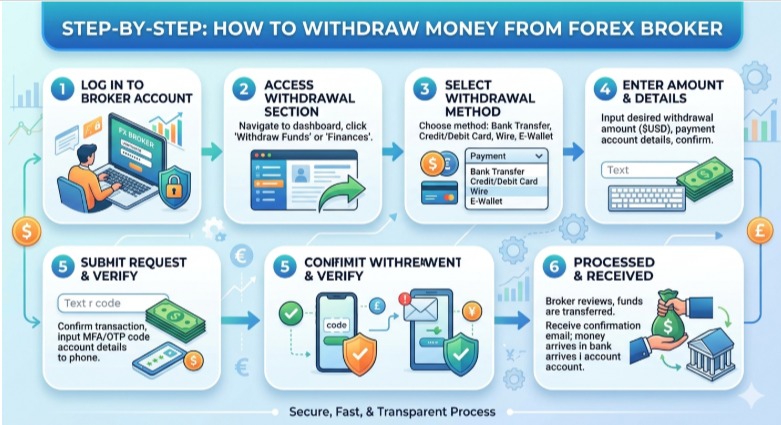

Step-by-Step: How to Withdraw Money from a Forex Broker

Step 1: Sign in and go to the withdrawal section.

Enter your trading account, and navigate to “Funds,” “Wallet,” or “Withdraw” in the dashboard.

Step 2: Select the After-Tax Method.

Choose the forex withdrawal options in India, which include bank transfer, UPI (domestic brokers), e-wallets, or wire transfer (international brokers).

Step 3: Keyboard in Amount and Bank Details.

Type in the amount of withdrawal and provide appropriate bank information, such as account number and SWIFT code (when sending money abroad). Minor errors will cause delays in payments.

Step 4: Finish the KYC check.

In certain cases, brokers might request PAN, Aadhaar, or bank documents to fulfill the request, particularly when making higher withdrawals.

Step 5: Confirm Request

Read all the information and make sure that it was used for OTP or email authentication.

Step 6: Processing Time

- Brokers in India (SEBI): 1-3 business days.

- Offshore forex brokers: 3-7 business days.

Step 7: Receive Funds

Deposit money is directly credited to your bank account. Record information to report on taxes (where necessary).

Forex Withdrawal Methods in India: Which One Should You Use?

1. Bank wire transfer (NEFT/RTGS/IMPS).

The most popular alternative. Domestic brokers resort to NEFT/IMPS, and offshore brokers prefer SWIFT transfers.

- Turnaround Time: 1-5 business days.

- Most suitable for: Large withdrawals.

- Limitations: There could be international charges.

2. UPI / Net Banking (Only Domestic Brokers)

Assisted by SEBI-approved applications such as Zerodha, Angel One, and Upstox to do instant withdrawals.

- Processing time: 24 hours or less to same day.

- Best use: Small withdrawals that are quick.

- Restriction: Only for Indian brokers.

3. e-wallets (Skrill, Neteller, PayPal)

Widespread among offshore forex brokers, but it is not readily available in India.

- Processing time: 24–48 hours

- Best when: Withdrawing between medium and large amounts.

- Limit: An additional conversion and service charges.

4. Cryptocurrency (USDT, Bitcoin)

Certain offshore brokers provide crypto withdrawals; however, these are affected by the volatility in the price and taxation in India.

- Time of processing: A few hours.

- The best: Advanced users will want to use it at a fast pace.

- Limit: Cryptocurrency and taxation regulations.

Forex Withdrawal Fees in India: What Will It Cost You?

In learning how to withdraw money from a forex broker, it is significant to comprehend the expenses to avoid unnoticed expenses.

| Withdrawal method | Typical fee |

| NEFT/IMPS (Domestic) | ₹0 – ₹25 per transaction |

| Skrill/Neteller | 1% – 3% of the amount |

| UPI (Domestic Brokers) | Usually free |

| International Wire Transfer | $15 – $40 per transfer |

| Cryptocurrency | Network gas fee (variable) |

Other charges to be monitored.

- Currency conversion charges: 0.5-2.0% markup on the conversion of USD to INR.

- Intermediary bank fees: $10-25 in case of SWIFT transfers.

- Inactivity charges: There are brokers that have inactivity charges.

Forex Withdrawal Rules India: Stay Compliant

1. LRS Limit

The Indian residents are allowed to remit USD 250,000 in a financial year under the Liberalized Remittance Scheme. Offshore funding, which is associated with withdrawals, should be effectively monitored.

2. Tax Reporting

In India, the Forex profits are subject to tax and should be reported in your income tax return under Schedule FA (Foreign Assets). It is categorized in terms of the trading frequency (business or speculative income).

3. FEMA Compliance

Any transaction in the forex should be in accordance with the Foreign Exchange Management Act of 1999. Tax authorities may take a closer interest in unexplained outflows or inflows of foreign countries.

4. Transfers of LRS on TCS.

In the case of remitting more than 7 lakh per annum, the TCS of 20% might be applicable according to the existing tax regulations when investing overseas in LRS.

Common Reasons Forex Withdrawals Get Rejected or Delayed

Despite taking all the steps in the right direction, withdrawals occasionally come to a wall. The most widespread are the following:

- Unverified KYC: In case the documents of your account are not up-to-date or complete, the broker might withhold the withdrawal.

- Banking mismatch: Such a simple mistake as an account number or IFSC can lead to a rejection.

- Active bonus terms: In many offshore brokerages, the terms of bonuses include trading volume conditions—failing to meet the conditions may prevent withdrawal of bonuses.

- Red flags: Huge withdrawals or abrupt withdrawals may lead to an internal compliance review.

- Regional limitations: There are regional limitations on withdrawals by users, caused by payment processing limitations by some brokers.

Tips to Make Your Forex Withdrawal Faster and Smoother

The following are some of the tips every Indian forex trader needs to adhere to:

- Be sure to maintain your KYC with your broker.

- Go to the same bank account you used to deposit the amount in—this will prevent AML flags.

- Do not withdraw during the weekends or bank holidays—the length of processing time increases.

- Keep a registry of any withdrawal certifications and FIRC certificates to pay taxes.

- You can use a small withdrawal when working with a new broker.

- Check broker withdrawal windows—there are those offshore brokers who do not handle withdrawals on any other day.

Conclusion

To learn how to withdraw money from Forex broker accounts in India, one must have an awareness of regulations, fees, and how to withdraw money appropriately. To facilitate smooth transactions, traders would have to adhere to the forex withdrawal rules India, select safe forex withdrawal procedures in India, and bear the forex withdrawal fees in India. By remaining within the guidelines of the RBI and FEMA, you can keep any delays, penalties, and account problems at bay and get your profits safely deposited into your bank account.

Learn how to withdraw money from a forex broker with confidence—learn more intelligent tricks of making money and trading in compliance today with Insightful Trade.

FAQs

- How long does forex withdrawal take in India?

In the case of SEBI-regulated brokers, it will take 1-3 business days, whereas offshore forex brokers will take 3-7 business days, depending on the procedure. The bank processing can also increase the time it takes to transfer a wire across borders.

- Is it legal to withdraw money from offshore forex brokers in India?

It is in a gray area of regulation of FEMA. The withdrawals should be made according to LRS limits (USD 250,000/year), and they have to be listed in your income tax filing as Schedule FA. It is advisable to talk to a CA.

- What are forex withdrawal fees in India?

There are usual domestic transfer fees of ₹10-25, wire transfer fees of 15-40, and e-wallet fees of 1-3%. There can also be the currency conversion charges of approximately 0.5%–2%.

- Can I withdraw forex money to UPI?

Yes, but only licensed brokers of SEBI. UPI is not supported by offshore brokers due to the restriction of RBI, and bank transfer is usually employed.

- Is forex profit taxable in India?

Yes. Forex income can be classified as business or speculative income, which is subject to tax and should be reported in your ITR in Schedule FA.

Author: Arihant Jain

Trading Experience: 5+ Years

Arihant Jain is a financial markets analyst and trading educator with expertise in Forex, indices, crypto, and risk-managed trading systems. His insights are based on real trading experience, data-driven analysis, and transparent market understanding. All content is reviewed for accuracy and aligns with Google’s EEAT guidelines.

Risk Disclaimer:

Trading involves substantial risk. All information is for educational purposes only and should not be taken as financial advice. Always do your own research.